Survivor Benefits 2026: Eligibility for Spouses & Children Under 18

Understanding 2026 Survivor Benefits is crucial for eligible spouses and children under 18 in the U.S., providing vital financial support after a wage earner’s death through Social Security programs.

Navigating the complexities of Survivor Benefits 2026 can be a daunting task, especially during a time of loss. These crucial Social Security benefits offer a financial lifeline to eligible family members, primarily spouses and children under 18, after a wage earner passes away. This guide aims to demystify the eligibility criteria, application process, and important considerations for securing these vital protections.

Understanding Social Security Survivor Benefits

Social Security Survivor Benefits provide essential financial support to the family members of a deceased worker who contributed to Social Security. These benefits are not merely a payout but a continuation of the worker’s earnings record, designed to help families maintain financial stability during a difficult period.

The program is a cornerstone of American social welfare, offering protection to millions of families. Eligibility often depends on the deceased worker’s earnings history and the relationship of the survivor to the deceased. The rules, while generally consistent, can have nuances, making a clear understanding imperative.

Who is covered by survivor benefits?

Survivor benefits extend to various family members, but the focus often remains on spouses and dependent children. The Social Security Administration (SSA) defines specific relationships and conditions that must be met for a claim to be considered valid.

- Spouses: Widows, widowers, and in some cases, divorced spouses may be eligible.

- Children: Unmarried children under 18 (or 19 if still in high school) and disabled children of any age.

- Parents: Dependent parents aged 62 or older may also qualify under certain circumstances.

Each category has distinct requirements, and understanding these can significantly impact the success of an application. The benefit amount is calculated based on the deceased worker’s lifetime average earnings, ensuring that those who contributed more receive a higher benefit.

In essence, Social Security Survivor Benefits are a critical component of financial planning and security for American families. Knowing the foundational aspects of this program is the first step toward ensuring your family is protected.

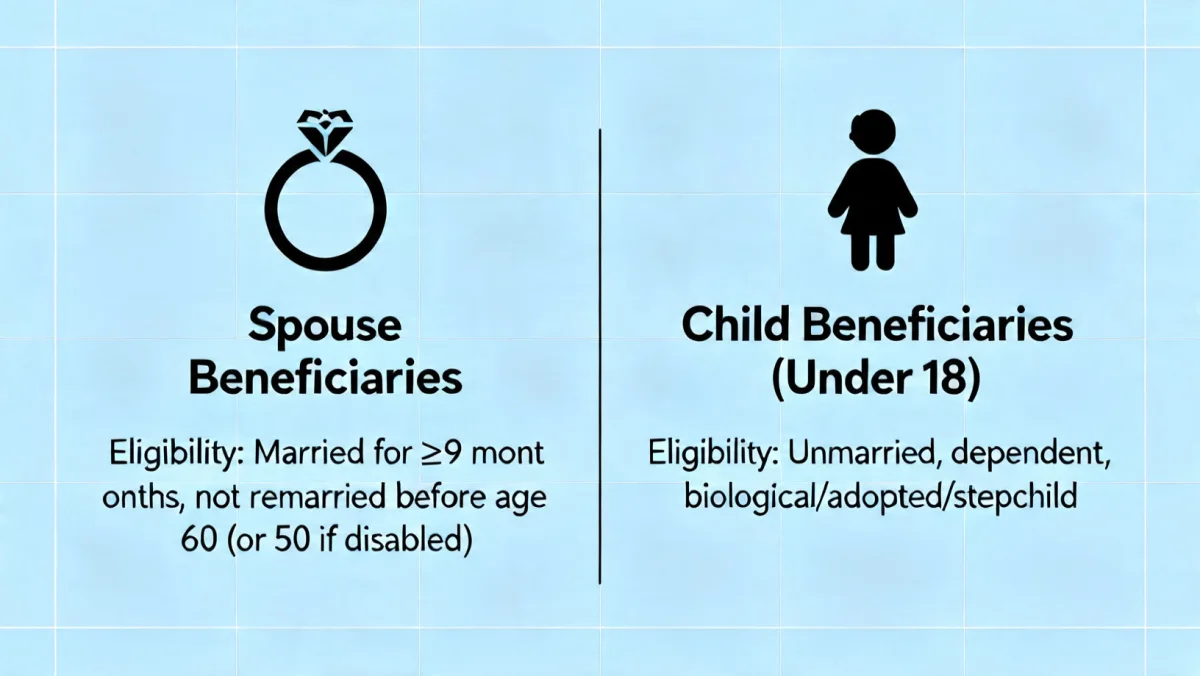

Eligibility Criteria for Spouses in 2026

For spouses, eligibility for Survivor Benefits in 2026 hinges on several factors, including age, marital status, and the presence of dependent children. These criteria are designed to ensure benefits are directed to those most in need of support after the loss of a spouse.

The rules recognize the varied circumstances of surviving spouses, offering different avenues for qualification. It’s important to differentiate between immediate and long-term eligibility, as some conditions may change over time.

Widows and Widowers

Generally, a widow or widower can start receiving benefits as early as age 60, or age 50 if they are disabled. If the surviving spouse is caring for the deceased’s child who is under age 16 or disabled, they can receive benefits at any age. This provision is particularly important for families with young children, providing crucial support during formative years.

- Age 60: Standard eligibility for non-disabled surviving spouses.

- Age 50: Eligibility for disabled surviving spouses.

- Any age: If caring for a child under 16 or disabled.

Remarriage can affect eligibility. If a widow or widower remarries before age 60 (or age 50 if disabled), they generally cannot receive benefits unless the later marriage ends. However, remarriage after age 60 (or age 50 if disabled) does not affect their eligibility for benefits from their deceased spouse’s record.

Divorced Spouses Eligibility

Even after divorce, a surviving divorced spouse may be eligible for benefits. The key requirements include having been married to the deceased worker for at least 10 years, not being remarried, and being at least age 60 (or 50 if disabled). The deceased worker must also have been entitled to Social Security retirement or disability benefits.

The rules for divorced spouses are often overlooked but provide a crucial safety net. It’s important for divorced individuals to understand these provisions, as they can represent significant financial assistance. The benefit amount for a divorced spouse is the same as for a widow or widower.

Understanding these specific criteria for spouses, both current and divorced, is critical for anyone seeking to claim Survivor Benefits. Each situation is unique, and careful review of the SSA guidelines is always recommended.

Eligibility Criteria for Children Under 18

Children play a significant role in the Survivor Benefits program, often receiving benefits until they reach adulthood or complete high school. These benefits are intended to provide financial stability for minors who have lost a parent, helping to cover living expenses and educational costs.

The criteria for children are relatively straightforward but have specific age and enrollment requirements. The SSA aims to ensure that children are supported during their dependent years, recognizing the financial impact of a parent’s death.

Dependent Child Requirements

To be eligible for Survivor Benefits, a child must be unmarried and:

- Under age 18.

- Under age 19 if a full-time student in elementary or secondary school.

- Age 18 or older and disabled, with the disability starting before age 22.

This includes biological children, adopted children, stepchildren, and in some cases, grandchildren, provided they were dependent on the deceased worker. The definition of ‘dependent’ is crucial and usually means the child was living with or receiving at least half of their support from the deceased worker.

The benefits received by children can significantly contribute to a household’s income, especially if the surviving parent is also receiving benefits. This combined support helps ensure that children’s needs are met without undue financial strain.

Impact of Education and Disability on Child Benefits

For children who are still in school, benefits can continue up to age 19, provided they remain full-time students in elementary or secondary school. This extension acknowledges the ongoing financial needs associated with education. Once a child graduates or reaches age 19, whichever comes first, their benefits typically cease.

For disabled children, the rules are more flexible. If a child’s disability began before age 22, they can receive benefits indefinitely, regardless of age, as long as they remain disabled and unmarried. This provision is vital for families caring for adult children with disabilities who rely on parental support.

It is important for guardians to keep the SSA informed of any changes in a child’s educational status or disability status to ensure continuous and appropriate benefit payments. The SSA periodically reviews cases to confirm ongoing eligibility.

The comprehensive support provided to children through Survivor Benefits underscores the program’s commitment to protecting the most vulnerable members of society during times of loss.

Applying for Survivor Benefits in 2026

The application process for Survivor Benefits can seem complex, but understanding the steps and required documentation can greatly simplify it. Timeliness is often important, as some benefits may be retroactive, but delays can impact the total amount received.

The Social Security Administration (SSA) provides various channels for application, aiming to make the process accessible during a sensitive time. Gathering all necessary documents beforehand can accelerate the review process.

Required Documentation

When applying for Survivor Benefits, you will need several key documents. Having these readily available will streamline your application. Typically, these include:

- The deceased worker’s Social Security number.

- Your Social Security number (and those of any children applying).

- The deceased worker’s death certificate.

- Proof of age for all applicants (birth certificates).

- Marriage certificate (for spouses) or divorce decree (for divorced spouses).

- Children’s birth certificates.

- Deceased worker’s W-2 forms or self-employment tax returns for the most recent year.

- Bank account information for direct deposit.

Additional documents may be requested depending on the specific circumstances, such as medical records for disabled applicants or school enrollment verification for students over 18. It is always wise to contact the SSA directly to confirm the exact documentation needed for your unique situation.

The Application Process

While you cannot apply for Survivor Benefits online, you can start the process by calling the SSA or visiting your local Social Security office. An appointment is often recommended for in-person visits to minimize wait times.

During the application interview, an SSA representative will guide you through the forms and help clarify any questions. Be prepared to provide detailed information about the deceased worker, your relationship, and your current financial situation. It is crucial to be honest and accurate in all information provided.

After submitting your application, the SSA will review your case. This review period can vary, but you will be notified of their decision by mail. If approved, benefits will typically begin shortly thereafter, retroactive to the month of application or the month of the worker’s death, depending on the circumstances.

Proactively gathering documents and understanding the application steps helps alleviate stress and ensures a smoother process for receiving crucial Survivor Benefits.

Factors Affecting Benefit Amounts

The amount of Survivor Benefits received is not uniform; it varies based on several factors, primarily the deceased worker’s earnings history and the number of eligible family members. Understanding these calculations can help beneficiaries anticipate the financial support they will receive.

Social Security aims to replace a portion of the deceased’s income, but there are limits to how much a family can receive. These limits are designed to balance support with the overall solvency of the Social Security system.

Deceased Worker’s Earnings Record

The primary determinant of the benefit amount is the deceased worker’s lifetime average earnings. The higher the worker’s earnings over their career, the higher their potential Social Security benefits, including survivor benefits. The SSA uses a complex formula to calculate the ‘Primary Insurance Amount’ (PIA), which is the base for all benefits payable on that record.

- High earners: Generally result in higher survivor benefits.

- Consistent employment: A long history of covered earnings contributes positively.

- PIA calculation: The foundation for determining individual and family benefit amounts.

Each eligible family member receives a percentage of the deceased worker’s PIA. For example, a widow or widower at full retirement age might receive 100% of the PIA, while a child might receive 75%. These percentages are standard across the program.

Family Maximum Benefit

While individual beneficiaries are entitled to a percentage of the deceased’s PIA, there is a limit to the total amount of benefits that can be paid to a family. This is known as the ‘family maximum benefit’. If the sum of all individual benefits exceeds this maximum, each individual benefit will be reduced proportionately until the total reaches the family maximum.

The family maximum benefit is typically between 150% and 180% of the deceased worker’s PIA. This cap ensures that while families receive substantial support, the system remains fiscally responsible. It’s important to note that if a divorced spouse is receiving benefits, their payments usually do not count towards the family maximum for the current family.

Factors such as working while receiving benefits (earnings limit) can also impact the amount received, especially for younger beneficiaries. Understanding these various influences is crucial for accurately estimating potential survivor benefits.

Important Considerations for 2026

As we look towards 2026, several important considerations can impact Survivor Benefits, from potential legislative changes to ongoing adjustments in cost-of-living allowances. Staying informed about these broader trends is vital for beneficiaries.

While the core structure of Social Security benefits tends to remain stable, minor adjustments and economic factors can influence the real value and accessibility of these payments. Proactive planning and awareness are always beneficial.

Cost-of-Living Adjustments (COLAs)

Social Security benefits, including Survivor Benefits, are typically subject to annual Cost-of-Living Adjustments (COLAs). These adjustments are designed to help benefits keep pace with inflation, maintaining purchasing power for beneficiaries. COLAs are usually announced in October and take effect in December for the following year.

The COLA for 2026 will depend on economic indicators closer to that time, particularly the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). While COLAs are not guaranteed to be substantial every year, they are a critical mechanism for protecting beneficiaries from rising costs.

Potential Legislative Changes

The future of Social Security is a perennial topic of discussion in Washington D.C. While major overhauls are less common, minor legislative adjustments can occur. These might relate to eligibility ages, benefit calculation formulas, or the earnings limit for those who work while receiving benefits.

- Benefit age adjustments: Possible shifts in full retirement or eligibility ages.

- Earnings limit modifications: Changes to how much can be earned before benefits are reduced.

- Funding discussions: Ongoing debates about the long-term solvency of the trust funds.

Beneficiaries and those planning for future benefits should pay attention to news from the Social Security Administration and legislative updates from Congress. Organizations advocating for seniors and families often provide valuable insights into potential changes.

Keeping abreast of these considerations ensures that individuals can make informed decisions and adapt their financial plans accordingly, maximizing the value of their Survivor Benefits.

Maximizing Your Survivor Benefits

While the rules for Survivor Benefits are set, there are strategies and considerations that can help eligible individuals maximize their financial support. Understanding your options and making informed decisions can significantly impact your long-term financial well-being.

This often involves careful timing of applications, understanding interactions with other benefits, and knowing when to seek professional advice. Proactive engagement with the SSA and financial planning resources can be invaluable.

Timing Your Application Strategically

For surviving spouses, the timing of when you apply for benefits can affect the total amount received. While you can apply as early as age 60 (or 50 if disabled), delaying your application until your full retirement age can result in a higher monthly benefit. However, if you are caring for a child under 16, applying immediately is usually advisable, as this benefit is not subject to age-related reductions.

Consider your current financial needs versus the desire for a higher future payment. If you have other sources of income, delaying might be a viable strategy. If immediate financial support is critical, applying sooner is the more practical choice.

- Early application: Provides immediate income, but benefits may be reduced.

- Full retirement age application: Maximizes monthly benefit amount.

- Child in care: Apply immediately for benefits for yourself and the child.

Coordinating with Other Benefits and Resources

Survivor Benefits may interact with other forms of income or benefits, such as a pension, other Social Security benefits (e.g., your own retirement benefit), or workers’ compensation. It’s crucial to understand how these might affect your survivor payments.

For instance, if you are eligible for both a survivor benefit and your own retirement benefit, you can typically choose to receive one first and switch to the other later if it results in a higher payment. Consulting with an SSA representative or a financial advisor specializing in Social Security can help you navigate these complex choices.

Additionally, explore other potential resources, such as employer-sponsored life insurance, veterans’ benefits, or state assistance programs, which can complement your Social Security Survivor Benefits. A holistic approach to financial planning ensures all available support is utilized effectively.

By carefully planning and understanding all available options, beneficiaries can ensure they are maximizing the crucial support provided by Survivor Benefits.

| Key Point | Brief Description |

|---|---|

| Spousal Eligibility | Widows/widowers can claim benefits at age 60 (50 if disabled), or any age if caring for a child under 16. |

| Child Eligibility | Unmarried children under 18 (19 if full-time student) or disabled before age 22 are eligible. |

| Application Process | Requires documentation like death certificate and SSNs; apply by phone or in person at SSA offices. |

| Benefit Calculation | Based on deceased worker’s earnings and subject to a family maximum benefit limit. |

Frequently Asked Questions About Survivor Benefits 2026

Eligible individuals include widows, widowers, and divorced spouses (under specific conditions), as well as unmarried children under 18 (or 19 if still in high school) and disabled children whose disability began before age 22.

Yes, a divorced spouse may be eligible if the marriage lasted at least 10 years, they are not remarried, and are at least 60 years old (50 if disabled). The deceased worker must have been entitled to Social Security benefits.

You cannot apply online. You must contact the Social Security Administration by phone or visit a local SSA office. It’s advisable to gather all necessary documentation before starting the application process.

If a widow or widower remarries before age 60 (or 50 if disabled), benefits generally stop. However, remarriage after age 60 (or 50 if disabled) does not affect eligibility for benefits from the deceased spouse’s record.

You will typically need the child’s birth certificate, the deceased parent’s Social Security number and death certificate, and proof of school enrollment if the child is over 18 but under 19 and still studying.

Conclusion

Understanding and securing Survivor Benefits 2026 is a profound way to ensure financial stability for families facing the loss of a loved one. The Social Security Administration’s program provides critical support to eligible spouses and children under 18, offering a safety net during challenging times. By familiarizing yourself with the eligibility criteria, the application process, and factors influencing benefit amounts, you can navigate these provisions effectively. Staying informed about potential legislative changes and maximizing your benefits through strategic planning are key steps in protecting your family’s financial future. This comprehensive guide serves as a valuable resource to help you understand and access the benefits you or your family may be entitled to.